Recent Fraud Threats in the UK & Ireland — What Every Business Needs to Know

Fraud remains one of the most pressing and fast-evolving threats to UK and Irish organisations. Over the past six months, new cases have underscored how even the most robust companies can be caught off-guard by increasingly sophisticated criminal tactics.

Below we highlight three major fraud threats that have dominated recent headlines — and what practical steps businesses in Northern Ireland can take to defend themselves.

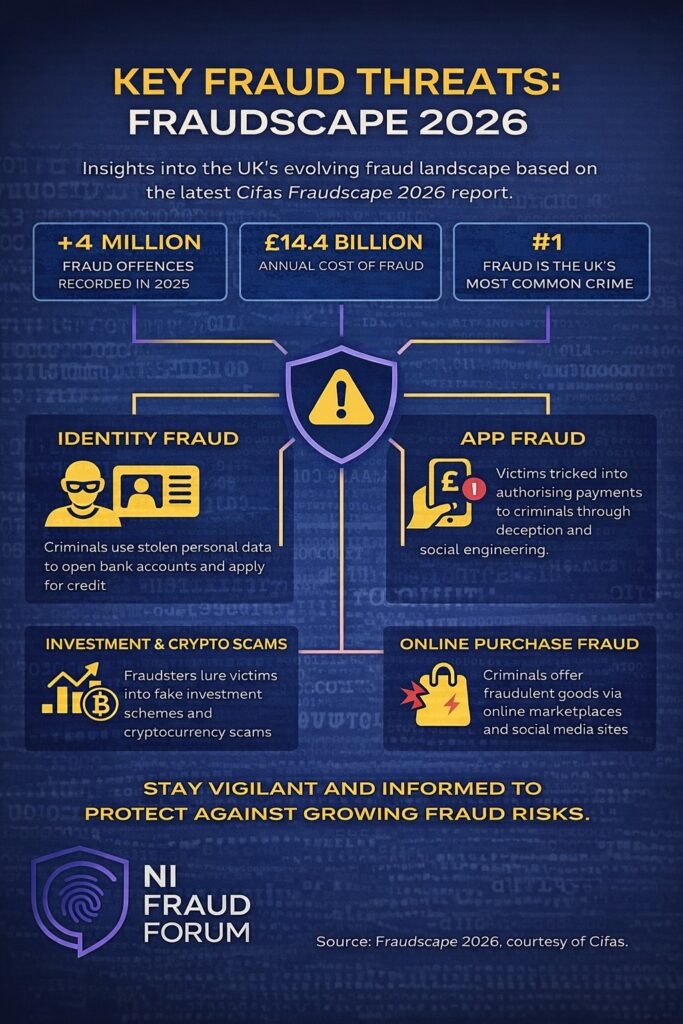

1. APP and Invoice-Redirection Fraud Still the #1 Threat

Authorised Push Payment (APP) fraud continues to top the league table of corporate losses. In March 2025, Santander UK successfully defended a High Court claim from a private education provider that had lost £415,000 through an APP scam — the court ruled that banks cannot be held automatically responsible for customer mistakes. Reuters coverage

Reuters coverage

Meanwhile, UK Finance reports that while total APP fraud losses fell to £450.7 million in 2024, criminals have simply shifted tactics toward impersonation, business email compromise (BEC), and look-alike domain fraud. The Guardian | Financial Times

2. Procurement and Construction Corruption — A Growing Menace

Procurement fraud and bribery cases continue to surface across the UK public sector. A recent Scottish case involving construction contracts across NHS health Boards exposed years of kickbacks, false invoicing, and insider collusion — a reminder that fraud can embed itself within legitimate supply chains.

For Northern Ireland’s construction, housing, and public procurement sectors, the message is clear: layered subcontracting and informal “favours” can quickly slide into corruption risk. Transparency, due diligence, and cultural vigilance are critical safeguards.

3. The New “Failure to Prevent Fraud” Offence (Effective Sept 2025)

From 1 September 2025, large UK organisations (and NI subsidiaries operating in the UK) face criminal liability if an employee, agent, or contractor commits fraud to benefit the organisation — unless “reasonable prevention procedures” are demonstrably in place. WilmerHale Analysis | Dechert Commentary

This will be a game-changer for Boards, requiring documented anti-fraud frameworks, training, and internal reporting — not just policy statements.

Practical Steps for Northern Ireland Businesses

Verify supplier bank changes via independent call-backs.

Apply dual authorisation for new payees and bank detail changes.

Strengthen email security — MFA, DMARC, and restricted shared mailbox access.

Conduct supplier due diligence: Ultimate Beneficial Owner (UBO) checks, tax/VAT verification, and adverse media screening.

Maintain whistleblowing channels that allow safe reporting.

Train staff regularly to recognise coercion, manipulation, and “social engineering.”

Document your anti-fraud framework — vital for the new Failure to Prevent Fraud defence.

Download our Free Checklist

We’ve prepared a one-page Procurement & Accounts Payable Anti-Fraud Checklist designed for use by finance and procurement teams.